Industry analyst firm, LightCounting has released its latest State of the Optical Communications Industry Report.

Amongst its findings, said the company, optical component and module vendors had the lowest profitability across all levels of the industry supply chain for the last 15 years.

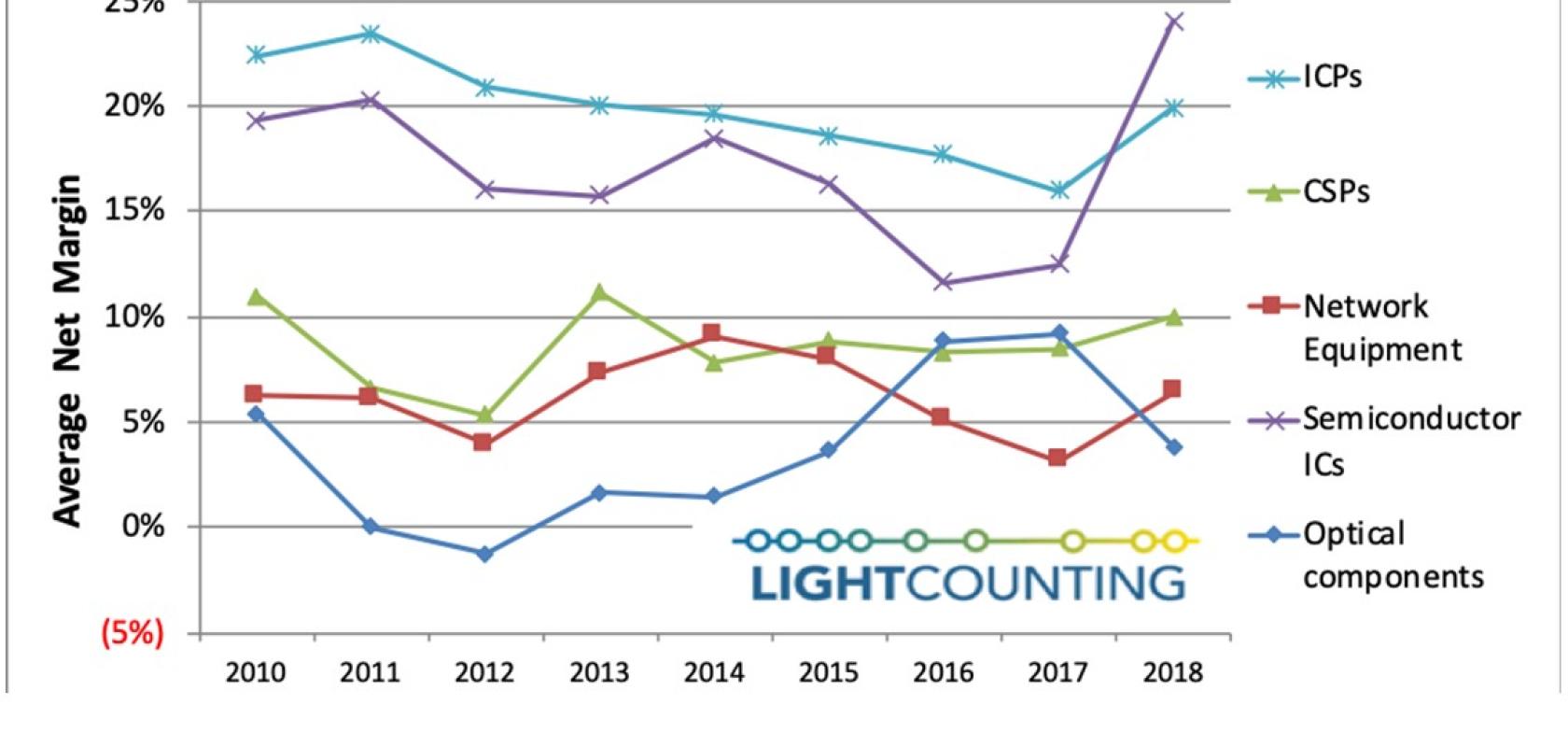

The group’s average profit margin improved in 2016-2017, reaching 9 per cent, but dropped to below 4 per cent in 2018. In contrast, profits of other company types in the industry improved last year. Demand for networking products, including optics was very strong in 2018. So, what is the problem with optics?

The main problem, said LightCounting, is that they are only a small part of a large industry. Combined revenues of ICPs and CSPs are more than $1.8 trillion, and those of network equipment manufacturers and semiconductor IC vendors are more than $300 billion and $200 billion, respectively. Sales of publicly traded manufacturers of optical components and modules reached just $7.2 billion in 2018. The net income of the optical component and module vendors was $0.27 billion, versus $111 billion for the CSPs in 2018.

The report highlights size as important when negotiating pricing, with sharp price declines for many optical products and especially for 100GbE transceivers erasing profits in 2018. Shipments of 100GbE transceivers more than doubled, exceeding 6 million units, but revenue increased only by 14 per cent last year. In comparison, sales of 100GbE products increased by 150 per cent and 45 per cent in 2016 and 2017, respectively. Supply shortages of some of 100GbE products helped sustain prices in 2016-2017 and resulted in improved supplier profitability. This is not the first time that profits of the suppliers picked up when their products were in short supply, noted the report.

The inability of suppliers to control pricing also stems from the lack of unique products and designs that can be protected by patents. Then there is the trade war between China and the U.S, which is described as a ‘wild card’. Tensions are reaching new heights and at the time of publication, it does not seem likely that U.S.-based suppliers will be able to sell products to Huawei, at least, for an unknown period of time. This is problematic for the majority of optical components suppliers, but companies that rely on Huawei for a high percentage of their revenues are in real danger.

Demanding customers, shorter product lifecycles and the large investments required to support development of new products all present continuing challenges to suppliers. Start-ups will continue to test the dominance of established vendors, and new technologies like Silicon Photonics (SiP) will accelerate innovation. In spite of this, LightCounting believes many suppliers of optical components and modules are on track for sustainable profitability in the next few years.

Projected demand for high-end products (200GbE, 2x200GbE, 400GbE) will continue to present new opportunities for these suppliers, but whether they will be able to make a profit remains to be seen. Future shortages may help, but the customer may choose not to deploy next generation optics until they are convinced that shortages in the supply chain can be avoided.

Lack of confidence in optics suppliers may be one of the reasons Cisco acquired Silicon Photonics (SiP) start-ups Lightwire and Luxtera, said the report. Ciena, FiberHome, Juniper, Huawei and ZTE are all investing more in internal manufacturing of optical components and modules and Intel is back in the optical transceiver business. Another motivation for recent interest in SiP startups may be that the optics is becoming an ever-larger portion of the bill of materials of networking systems, and a third could be the eventual co-packing of optics and ASICs, requiring a more intimate design relationship. All these factors would lead to equipment makers to want to have more control over the optics they use.

LightCounting cites that ‘there has to be a better way’. Lumentum sold its datacom transceiver business to Cambridge Industries Group (CIG) in March 2019, refocusing the company on its higher margin DWDM products and laser chips business. Using semiconductor laser technology to serve multiple markets, such as communications, facial recognition sensors, LIDARs, medical and industrial applications seems to be Lumentum’s strategy for the future. Once the acquisition of Finisar by II-VI Photonics is closed, the new company is likely to refocus its business as well. Serving multiple market segments using the same core chip technology works well in the semiconductor IC business. LightCounting asked, can this work well in the laser business?